https://www.tvbeurope.com/features/emea-tv-market-outlook

Findings from PwC’s recent Entertainment and Media Outlook suggest that advertising and electronic home video will drive growth in the EMEA Television market over the next five years. Adam Edelshain, senior manager in PwC’s entertainment and media team, details his analysis for TVBEurope.

BY CONTRIBUTOR

PUBLISHED: AUGUST 1, 2014

Findings from PwC’s recent Entertainment and Media Outlook suggest that advertising and electronic home video will drive growth in the EMEA Television market over the next five years. Adam Edelshain, senior manager in PwC’s entertainment and media team, details his analysis for TVBEurope.

Online TV advertising is expected to more than treble over the next five years, growing at a compound annual growth rate (CAGR) of 29.3 per cent to reach €1.6 billion by 2018. Over the same period, multi-channel broadcast advertising revenue is expected to grow at a CAGR of over ten per cent, taking it from €6.7 billion in 2013 to €10.9 billion by 2018.

Meanwhile, even more impressive growth rates are being witnessed in the electronic home video market. Total OTT/Streaming revenue grew by 46.6 per cent last year and is expected to continue to grow at a similarly impressive rate over the next five years. This growth is being spearheaded by Subscription Video On Demand (SVOD), which is expected to overtake Transactional Video On Demand (TVOD) this year and reach €2.3 billion by 2018. However, TVOD is growing very quickly as well, with annual growth of more than 30 per cent expected over the next five years. The strength of the OTT/Streaming market in EMEA is underlined by the fact that revenues from the OTT/Streaming electronic home video market will overtake Through-TV-Subscription revenues in 2017, a market which itself is expected to see double digit annual growth between now and 2018.

PwC’s E&M Outlook, which makes five-year projections for both advertising and consumer spending, has highlighted that the television market will grow at 3.4 per cent per year over the next five years. This will be a boost to the industry, which has seen significantly slower growth in 2012 and 2013. In fact, total TV advertising revenue fell in 2012 and grew only 0.4 per cent in 2013. Similar patterns were witnessed in the home video market, with revenues falling in 2012 and only growing at 0.6 per cent in 2013.

So what is driving this expected upturn in the EMEA television market?

There is no doubt that some of this growth can be attributed to the global economic recovery which has seen investor and consumer confidence return, to some extent. However, there are several other factors that are also key to this growth.

i. Growth of internet access

The first is the continued rapid growth of internet access even in the relatively mature markets of Western Europe. Globally, internet access is expected to generate more consumer spend than any other media product or service in the next five years. And this consumer spend will extend to the television market, driving revenue growth in online television, OTT/streaming and electronic home video.

In some markets, analysts have expressed concern that an increase in internet access revenue will divert spend away from consumer products. However, the growth of internet access itself is being driven by an increase in the size of its customer base. Fixed broadband penetration in EMEA will grow from 53.6 per cent to 61.6 per cent, while mobile internet growth will see penetration rise from 32.1 per cent to 58.3 per cent.

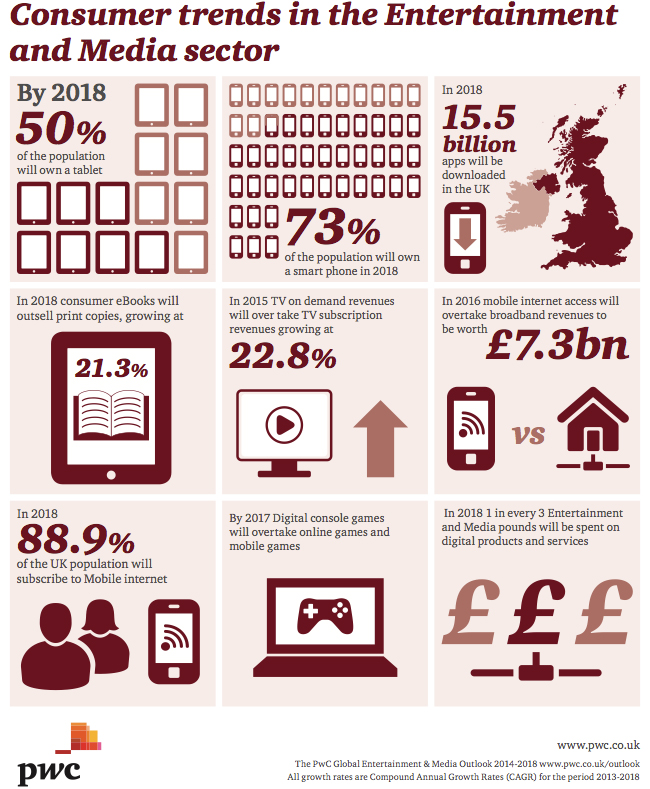

Accompanying growth in internet penetration is the strong increase in device ownership. Tablet ownership in EMEA will rise from 88 million in 2013 to 346 million by 2018, while smartphone ownership will more than double in the same period from 442 million in 2013 to 956 million devices by 2018. The increase in the number of consumers accessing and consuming digital products across an ever growing number of devices provides the television market with the perfect platform to grow its Online TV, OTT/Streaming and electronic home video offerings, while also driving growth in the digital TV advertising market.

ii. Shift in consumption habits towards ‘24/7 access’ and micro-transactions

Alongside the growth in internet access penetration and devices, there has also been a notable shift in consumption habits towards ‘24/7 access’ and micro-transactions. Consumers expect to be able to access high quality and (where relevant) tailored content whenever it suits them. This shift has been reflected by many businesses that have seen the need to adapt and develop consumer-centric business models. They have noted that the key to monetising the digital consumer is to adopt flexible business models that offer more choice and better experiences. This has been epitomised by the rapid growth seen in ‘on demand’ services such as the electronic home video over-the-top (OTT)/streaming sector, and, in particular, the rise of streaming video company Netflix. Investors’ confidence in OTT streaming services was underlined by the surging price in shares for Netflix in 2013. Its shares rose by almost 300 per cent in value during the year.

iii. Key digital markets gaining critical mass

Another aspect of growth in the EMEA broadcasting market is the fact that key digital markets are gaining critical mass. Fast growth rates in digital advertising, online TV and electronic home video were easy to overlook in the past because the revenues they generated were still very small.

However, this is no longer the case in some key markets. A major tipping point was reached in 2013 in the home video market. After falling in 2011 and 2012, the market experienced growth overall as declines in physical home video revenues were being replaced by electronic home video revenues. Electronic home video represented 9.6 per cent of the EMEA home video market in 2009, but this more than doubled to 22.8 per cent in 2013 and is expected to reach almost 50 per cent by 2018.

EMEA broadcasting market

Finally, it is important to note that growth of the EMEA broadcasting market is not evenly spread between Western Europe, Eastern Europe, the Middle East and Africa, or even within these segments.

Globally, key drivers for growth in entertainment and media are those countries where the internet access and device penetration have the opportunity to grow the fastest and this is consistent within EMEA.

In the TV advertising markets, Middle East and African countries are expected to grow at an average CAGR of 12.1 per cent, compared to three per cent in Western Europe, and seven per cent in Central and Eastern Europe. The picture is similar for TV subscriptions and licence fees, while in home video, Central and Eastern Europe is expected to grow even faster than the Middle East and Africa, driven by the growth of the Russian home video market, which is expected to grow at over 20 per cent annually over the next five years.

The big three players in the EMEA market, Germany, France and the UK, will all see much less spectacular growth rates. In TV subscriptions and licence fees, the three countries are expected to grow at a CAGR of between 1.4 per cent and 2.5 per cent over the next five years. In the home video market, France will grow at an impressive nine per cent CAGR from 2013 to 2018, overtaking Germany in 2017 to become the second largest home video market in EMEA. It will generate total spend of €2.3 billion by 2018, behind only the UK which will grow at 3.7 per cent annually to reach €3.6 billion by 2018.

In TV advertising spend, the UK will see the fastest CAGR of the three countries over the next five years, with 3.5 per cent annual growth expected. Here, though, the dominance of the ‘big three’ will be blown apart as France and Germany are overtaken by Russia in 2014 and 2018 respectively, a result of Russia’s large population, rapid growth of internet access penetration and the fact that TV is the only platform with truly national reach.

Yet, while there appears to be a positive growth story for the broadcasting market in EMEA, not every country is expected to benefit. Spain’s TV advertising and TV subscriptions revenue are both expected to decline over the next five years. And other countries, including Ireland, Belgium, Finland and Holland could see declines in their home video markets.

TV as a platform will also lose advertising market share in EMEA over next five years. Total TV advertising spend will be overtaken by internet advertising spend as the largest EMEA advertising market segment in 2015.

The industry is still to make much progress on the issue of TV audience measurement. While digital audiences are easier to identify and track, the growth of multi-channel and terrestrial TV in EMEA highlights the importance of knowing who and how big the audiences are in order to monetise them effectively.

Yet, it will be some comfort to all of those working in the industry that such issues are being addressed against a broad backdrop of growth over the next five years.